At a time when most industries are suffering from the economic stresses of the global coronavirus pandemic, the KYC industry is enjoying solid growth. Travel restrictions and social distancing rules are forcing businesses to conduct most of their work and client interaction remotely.

This, however, requires proper authentication and identity verification, and that fuels the growing interest in KYC solutions. How can this trend influence the financial industry, and which trends in KYC are we going to see in the nearest future? took a closer look at the KYC sector.

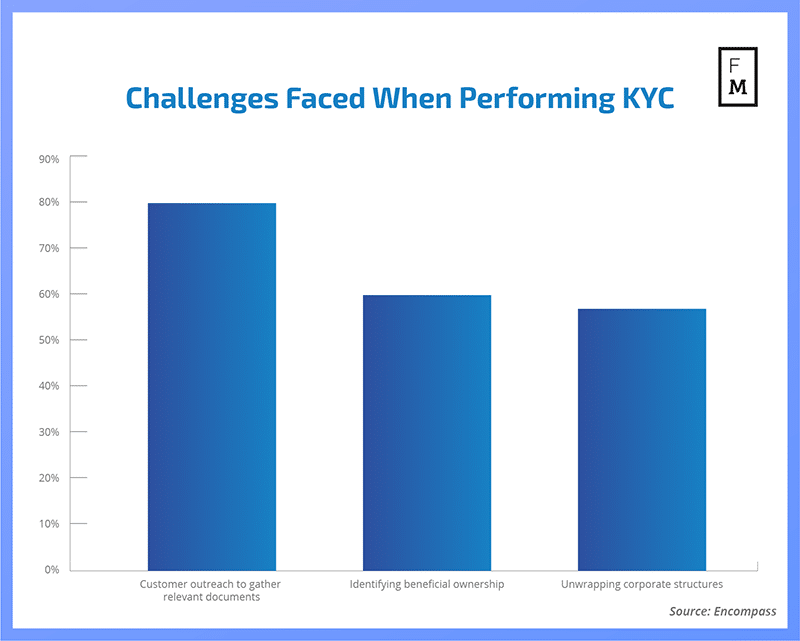

Looking at the current financial industry, one can see how the KYC sphere has evolved. The changes are seen on three different levels — first of all, the regulatory level. It is obvious today that a stringent KYC policy is one of the key elements of a sound financial environment in most countries. From a regulatory perspective, it allows for combating possible financial crimes better. The more reputable a given regulatory regime is, the more it will demand from industry participants when it comes to collecting information on their clients.

Victor Fredung, CEO of Shufti Pro, shared with Finance Magnates his observation on this matter: “KYC has changed significantly over the last five years. There have been many regulatory and technological advancements,” he said. “Also, there has been a rise in KYC compliance awareness among businesses. Some new regulations are passed, such as AMLD5 of EU, and several amendments are made in previous laws/recommendations by FATF and national authorities such as FINMA, FINCEN, FINTRAC, etc.”

Automation in KYC solutions

Today, everything in the KYC sphere is more automatic and is being taken care of by specialist or tailored software. Automation procedures seem to be more important today than ever before. With the COVID-19 pandemic paralyzing world economies, special measures had to be taken. One of them was social distancing, which is the main tool in combating the pandemic. This, of course, had to influence the way business is being conducted.

The coronavirus pandemic made people more aware of how quickly many things can be done without leaving your home or office. It also made people more aware of how serious the security of financial transactions and agreements should be taken. All of these developments had been growing slowly in the and will now speed up because of the pandemic.

What we want to see is minimal input from customers and more innovative financial businesses. The leverage of multiple sources to validate the data provided by the customers will be seen more often.

To get the full article and the bigger-picture perspective on how the industry evolved in 2019, get our latest Quarterly Intelligence Report.

KYC Industry Sees Spike in Demand Driven by COVID-19

Per Quarter

€510

1 issue per Year

–

Digital Version delivered to your email

Annual

€1,780

4 issues per Year

–

Digital Version delivered to your email

Published in Analysys

admin_mm

More from AnalysysMore posts in Analysys »

Be First to Comment